Letter to Shareholders

My grandfather Gianni Agnelli once told me: “Difficulties are not meant to stop us, but to test whether we have the resilience to endure the pain and the courage to continue.”

The past twelve months demanded that kind of resolve. Externally, volatility in global markets, tariffs and regulatory uncertainty created a complex operating environment for many of our companies. Internally, some of them also had to confront challenges of their own making, rooted in prior operational and strategic choices.

In many respects, 2025 was shaped by the actions to address issues that had emerged during 2024. It was a year spent working through those challenges deliberately and responsibly. Diagnosing problems, taking ownership where needed, and beginning the work of correcting course. Share prices across parts of our portfolio reflected these combined pressures, and Exor’s trading discount widened over the year.

We emerged tested but more determined, more disciplined, and more resilient.

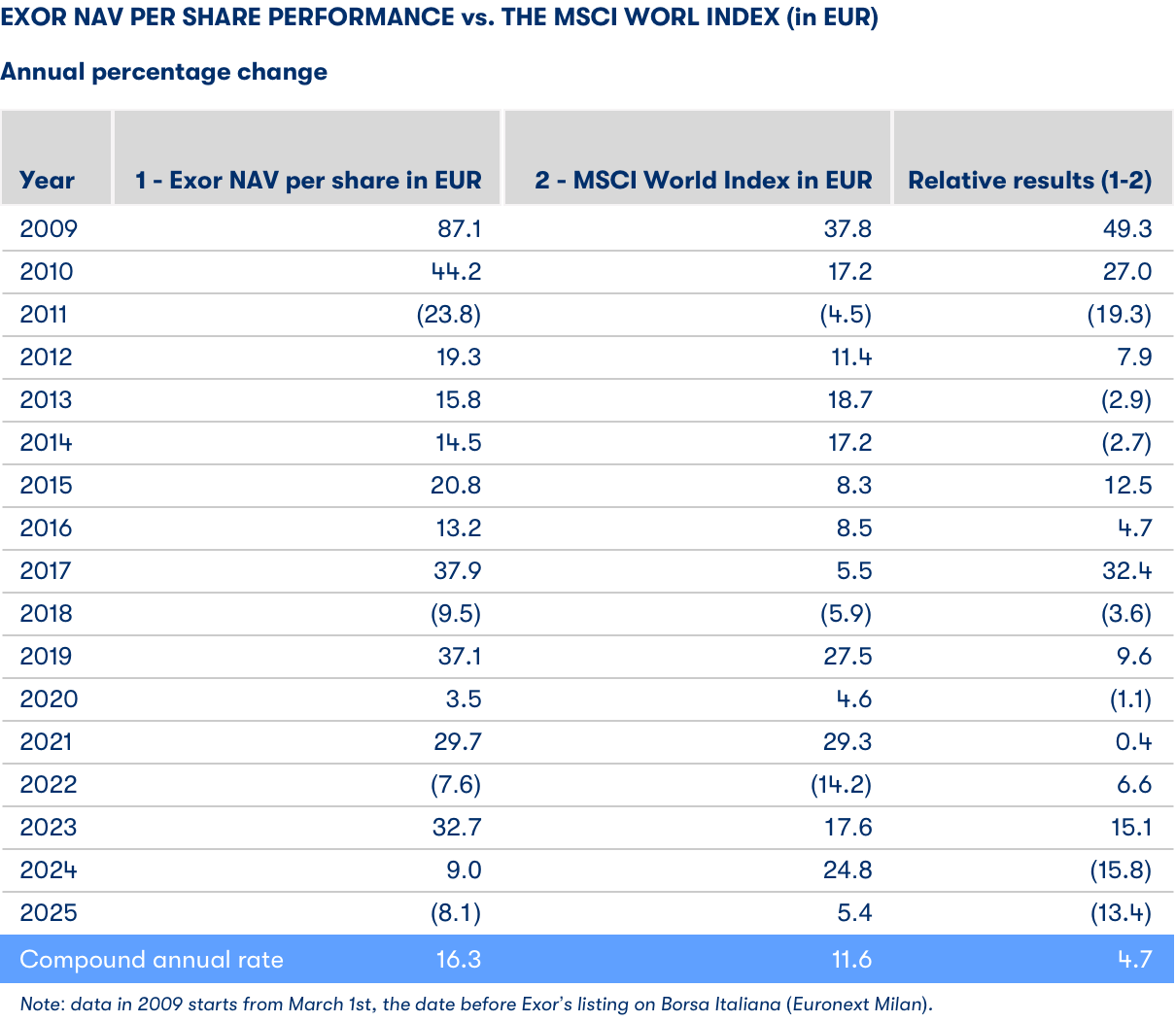

Exor in 2025

In 2025, Exor’s Net Asset Value (NAV) per share decreased by 8.1% underperforming our benchmark, the MSCI World Index, which increased by 5.4%.

Companies

Exor’s purpose is to build great companies. Around 80% of our portfolio consists of companies in which we are the reference shareholder and play an active role on their boards.

Stellantis: A year of reckoning and reset

I want to begin with addressing Stellantis, which experienced its most difficult year, marked by a record loss and a significant decline in value. It was a demanding twelve months, shaped both by external pressures and by the need to reassess certain internal decisions made in prior years.

On the external front, regulatory changes and tariffs created headwinds across markets. Internally, aggressive cost-cutting constrained the company’s ability to deliver vehicles at the pace and quality standards our customers deserve. We also moved toward electrification faster than consumer demand ultimately warranted, against a backdrop of shifting regulatory frameworks. In doing so, we drifted too far from customer preferences, and the adjustment that followed has been severe.

The lesson has been stark. In 2023, Stellantis delivered record net revenues of €189.5 billion and a net profit of €18.6 billion. In hindsight, that performance proved unsustainable, as just two years later results deteriorated sharply. Net revenues fell to €153.5 billion last year, while the company reported a net loss of €22.3 billion.

That swing underscored how quickly performance can shift in a complex industrial enterprise and how essential it is to maintain operational discipline and proximity to customers.

As a result, 2025 became a year of reckoning. A year spent examining every part of the organisation to identify areas of improvement and begin fixing them decisively.

As Chairman and, for the first half of the year, acting Chief Executive Officer, I worked at a pace that was both demanding and energising, alongside the Stellantis leadership team, colleagues across the organisation and the Board. I spent hundreds of hours travelling to plants, engineering centres and facilities around the world, engaging directly with teams and listening closely to understand where the company was falling short and where it needed to change.

During my time as acting CEO, I prioritised rebuilding relationships with our stakeholders, including dealers, suppliers and unions, and shifting the conversation from how to divide the cake to how we make it bigger in the first place.

I also placed particular emphasis on strengthening rigor around quality and on fostering an environment in which issues could be raised directly and addressed constructively. At one plant visit in Detroit, we were holding a discussion focused on persistent quality challenges on the shop floor. As the conversation unfolded, one member of the quality team said something that stayed with me: “We are finally able to speak up openly about what isn’t working and how to fix it.”

What mattered most was not the specific issue being discussed, but what that moment represented: a shift toward engagement and problem-solving. Creating the conditions for that change was an essential first step in reinforcing operational discipline across the company.

After careful consideration, the Board appointed Antonio Filosa as Chief Executive Officer, recognising his deep understanding of the company, broad industry expertise, and shared conviction that collaboration and accountability are the foundations of lasting progress.

Over the course of the year, Stellantis undertook a profound transformation: reorganising around regional structures, restoring rigor around quality, refocusing on the fundamentals of engineering, manufacturing and sales, and strengthening responsibility throughout the organisation.

Throughout 2025, the company focused on confronting legacy issues and preparing the ground for a broader reset, which was formally announced under Antonio’s leadership in February 2026. After complexity had increased and misalignments with customer preferences had grown, decisive action was required. This included a comprehensive clean-up of the balance sheet. In 2025, Stellantis recorded unusual charges of approximately €25 billion, reflecting difficult but necessary decisions to address past assumptions and restore strategic flexibility.

These charges were primarily driven by a strategic shift to place freedom of choice for customers at the centre of the company’s plans across electric vehicles, hybrids and advanced internal combustion engines. While the financial impact was significant, taking these actions helped reduce risk, prevent deeper dislocation, and create a clearer foundation from which the reset could be executed with credibility. In the meantime, Stellantis will continue to be at the forefront of the development of electric vehicles. That journey continues at a pace that needs to be governed by demand rather than command.

I am confident that Stellantis will turn the corner. With the changes already implemented and the renewed focus on execution and product excellence, the company is positioned to build exciting vehicles, rekindle its innovative spirit and continue to delight customers around the world.

Ferrari builds on its uniqueness

Ferrari delivered a strong financial performance in 2025. Net revenues increased by 7% year over year to €7.1 billion, EBIT rose by 12% over the same period, and profitability remained exceptional, with an EBIT margin of 29.5%. Demand for Ferrari’s products remains very solid, with the order book extending toward the end of 2027, reflecting the strength and uniqueness of the company’s offering.

Still, market sentiment toward Ferrari shifted over the year, reflecting different expectations around growth following the Capital Markets Day in October. The company’s share price reacted to concerns that its growth trajectory might prove softer than some investors had hoped. But our conviction in Ferrari rests not on short-term expectations, but on the quality of the emotional experiences it will continue to provide.

If something is to last, it must grow steadily. That principle is a discipline that allows Ferrari to create products of extraordinary distinction by remaining in control of how it grows. The task is to ensure that this long-term logic is clearly articulated and consistently executed, even when markets oscillate between patience and impatience.

At the Capital Markets Day, Ferrari also presented its 2030 Strategic Plan, providing clear visibility on the path ahead. The plan envisages an average of four new car launches per year between 2026 and 2030, and a strong product mix capable of sustaining total revenues of around €9 billion and EBITDA of at least €3.6 billion by 2030. These objectives reflect a disciplined approach to growth, balancing expansion with sustainable profitability.

On the sporting side, 2025 offered both triumphs and lessons. Ferrari delivered a remarkable year in endurance racing, winning both the World Endurance Championship manufacturers’ and drivers’ titles, securing another victory at Le Mans, and capturing the GT3 World Cup in Macau. These successes, coming more than half a century after Ferrari’s last endurance world title, reflected the extraordinary team spirit that unites everyone involved, from the mechanics in the pit lane to the engineers and drivers, working with shared dedication toward a common goal.

The decision to return to endurance racing was taken during the difficult period marked by the isolation of COVID, making the opportunity to celebrate these victories together again at the track all the more meaningful. Equally significant is the fact that, following this decision, Ferrari returned to win the centenary edition of Le Mans, fifty years after it last took part in the race, and went on to secure three consecutive wins with three different driver line-ups, a testament to the unity and collective strength of the team.

Formula 1, by contrast, fell short of ambitions. But Ferrari has always understood that racing is as much about learning as winning. Ferrari’s founder Enzo Ferrari kept what he called a “museum of mistakes,” a cabinet of broken parts collected in pursuit of progress. That mindset remains essential today: accountability and the determination to return stronger.

The year also underscored Ferrari’s commitment to the future through bold, long-horizon investments: the launch of the M-TECH Alfredo Ferrari educational hub in Maranello to train the next generation of innovators, the christening of the Hypersail project as the Prancing Horse adds the sea to the track and the unveiling of the revolutionary architecture behind the Ferrari Luce, the first full-electric Ferrari.

For Exor, Ferrari exemplifies what long-term stewardship can achieve. Short-term market reactions will ebb and flow. What matters more is that the company continues to invest in talent and technology, while preserving the rare balance between growth and uniqueness that has defined its success for generations.

This gives me an opportunity to reflect on the past decade, which began with Ferrari’s transition from a subsidiary to a public company following its listing in 2015. At the time, some questioned whether a company built on emotions could succeed under the discipline of the capital markets. Ten years later, the result is clear: Ferrari is a much stronger company. Our revenues have more than doubled since listing, rising from €2.85 billion to €7.15 billion last year. Our profit has jumped by 451% to €1.60 billion over the same period. Our market value has grown more than sixfold, reaching over €50 billion.

During this same period, my own involvement with Ferrari deepened. From Vice Chairman to Chairman, and for a time serving as acting CEO, I took on increasing responsibility as the company invested billions in capital expenditure, filed hundreds of patents, launched dozens of new cars and more than doubled its workforce, while remaining true to its DNA. These achievements are the result of the passion and dedication of the people of Ferrari and provide a strong foundation for the company’s continued success in the years ahead.

That is the lens through which we assess Ferrari today: a unique company defining its next decade through passion, innovation, and craftsmanship.

Philips executes with precision

2025 was a year of solid execution and renewed clarity for Philips, achieved against a challenging external backdrop. The company navigated headwinds including U.S. tariffs, slower demand in China, weakness of the U.S. dollar and heightened global competition, while continuing to invest in innovation and simplifying its operating model.

The full-year results reflected this progress. Philips’ sales rose by 2%, and the company reported a strong order intake growth of 6%, the highest level since 2020. Demand momentum was seen across different business units and particularly clear in its champion segments like Image Guided Therapy, Ultrasound, Monitoring and Personal Health. Beyond this, the company also expanded profitability with an adjusted EBITA margin of 12.3% and generated solid free cash flow.

The company took another step forward toward resolving the uncertainty surrounding the Respironics recall. Following its 2024 agreement with the US Department of Justice and the Food and Drug Administration, Philips paid a €1 billion settlement in 2025 and is focused on meeting the milestones set out in the Consent Decree. Quality remains Philips’ top priority as it works to close the remaining matters related to the Respironics recall, including the ongoing DOJ investigation.

Innovation continues to be a core strength of the company, with €1.7 billion invested in R&D last year. Recent product launches and the acquisition of SpectraWAVE have reinforced its position in key clinical segments. Among these breakthroughs was the unveiling of the BlueSeal Horizon, which will be the world’s first helium-free MRI 3.0T platform. By eliminating the need for helium refills and vent pipes, this technology dramatically simplifies installation while reducing operational complexity and environmental impact.

Her Majesty Queen Máxima of the Netherlands officially opened Philips’ new global headquarters in Amsterdam. The opening showcased the company’s latest technologies across imaging, image-guided therapy, smart patient monitoring and personal health, highlighting Philips’ focus on delivering more precise, connected and accessible care worldwide.

At its Capital Markets Day in February 2026, Philips outlined clear targets for 2026-2028, including mid-single-digit comparable sales growth CAGR over the three-year period, a mid-teens adjusted EBITA margin in 2028 and more than €4.5 billion in cumulative free cash flow through 2028. The market responded positively, demonstrating growing confidence in the company’s direction.

Over the course of 2025, Exor increased its stake in Philips to over 19%, reflecting our conviction in the company’s strategy and long-term positioning. The investment has delivered an annualized return of nearly 12% and the stock has overperformed its peers since our first investment in the company. We believe Philips is well placed to benefit from powerful trends shaping global healthcare.

CNH prepares for the cycle ahead

2025 was a tough year for CNH as the agriculture industry continues to face a cyclical downturn. Revenues declined 9% to $18.1 billion on lower industry equipment demand. Still, the company used the cycle to sharpen execution, strengthen the operating model and reinforce the foundations for the next phase of value creation.

At its Investor Day in May, CNH presented its Path to 2030, a focused strategy aimed at boosting product and technology leadership, expanding margins through the cycle and delivering durable shareholder returns. Innovation remains central to this effort. In 2025, CNH invested over $850 million in R&D, launched more than 50 agriculture and over 20 construction products, and continued to scale precision and automation technologies across its portfolio.

The company also worked closely with dealers to reduce new equipment inventories by approximately $800 million, while removing around $230 million of costs from the Agriculture segment through targeted quality, manufacturing and sourcing initiatives. These actions position CNH to emerge from the downturn more efficient, resilient and aligned with long-term demand.

Given persistent challenges in the agricultural equipment market, CNH is preparing for lower demand levels in 2026 ahead of an expected industry recovery in 2027.

Fifty years of Iveco and a new chapter

In 2025, Iveco Group reached a defining milestone, marking half a century of industrial heritage, alongside defining the next chapter of its evolution.

Reflecting on its history, the name IVECO was born in 1975. It is an acronym for Industrial Vehicles Corporation and was the result of the merger of five truck brands within Fiat, namely Fiat, OM and Lancia (Italy), Unic (France) and Magirus Deutz (Germany). This was followed by further European consolidation when Iveco acquired Ford Truck, Astra and Pegaso. In 1999, IVECO’s bus activities entered a joint venture with Renault’s bus activities to create Irisbus that would eventually become the fully owned business unit IVECO BUS.

In 2011, following the demerger of Fiat Group’s industrial activities, IVECO together with FPT Industrial (powertrains) become part of Fiat Industrial, that would later merge with CNH Global to create CNH Industrial. In 2019, CNH Industrial announced plans to demerge its on-highway activities resulting in the creation of two distinctly focused global leaders, one in sustainable agriculture and construction and the other in sustainable transportation and propulsion: Iveco Group.

When Iveco Group was officially listed in 2022, its valuation stood at €3.1 billion. As market confidence in Iveco Group’s ability to deliver grew, we supported the company in exploring different options for its future to build on its success and give a company that is relatively small within its industry greater scale.

This exploration led to the announcement in July 2025 of a new strategic direction for Iveco Group. This entails the sale of its defence business to Leonardo, enabling that division to engage in the consolidation shaping the European defence sector. At the same time, Iveco Group’s commercial vehicles (trucks and buses) and powertrain businesses would be combined with Tata Motors. United, Tata Motors and Iveco Group will create a new global player in the commercial vehicles sector. Their combination brings together complementary capabilities and international reach. Importantly, Tata Motors is committed to preserving the jobs, culture and brands of Iveco Group. This outcome offers real benefits for Iveco Group’s employees, customers, dealers, suppliers and its shareholders, with the combined transactions valuing the company at €5.3 billion.

I would like to warmly thank the Iveco Group management and employees for how smoothly they have been handling these processes to ensure the best outcomes for everyone.

As Iveco Group’s largest shareholder, Exor supports this new direction. We believe these transactions provide the company and its defence business with the scale and investment capacity they need, while safeguarding their place in the market and their heritage. As Iveco Group transitions from its first 50 years to its next, having overseen its successful evolution from an industrial division into a strong standalone public company, we believe it is well-positioned for the future.

Juventus rebuilds foundations for lasting success

Juventus has come through a difficult period in recent years, shaped by internal and external pressures that inevitably affected performance. We took ownership where it was required, stood firmly behind the club, and worked closely with its leadership to restore stability and put Juventus back on a constructive path following the resolution of its legal and regulatory matters.

Against this backdrop, 2025 was a year of laying the foundations for sustainable performance both on and off the pitch. We supported the club through our pro-rata contribution in a capital increase of nearly €100 million and backed important changes in its leadership.

On the sporting side, the women’s team delivered an outstanding season, securing a domestic double as Serie A champions and Coppa Italia winners. In January 2026, Juventus Women also won the Italian Super Cup. The men’s team has also begun to show progress following the appointment of Luciano Spalletti as head coach in October. Spalletti has brought renewed energy to the locker room, restoring the hunger and determination to win.

Off the pitch, financial performance improved meaningfully. In 2025, Juventus revenues increased by 34% year over year to €530 million, driven primarily by the men’s team’s return to the UEFA Champions League. Consequently, the club’s loss dropped by 71% compared to a year earlier to €58 million, with the company continuing on its path toward financial sustainability. During the year, the club also renewed its partnership with Adidas until the 2036/37 season for a total value of €408 million and extended its front-of-shirt sponsorship agreement with Jeep until June 2028 for €69 million.

In early 2026, Juventus also extended the contract of next-generation talent Kenan Yildiz through 2030, reaffirming our commitment to developing and retaining the club’s brightest prospects. This approach reflects our enduring conviction in Juventus. Exor remains a proud owner of the club, continuing a relationship that has spanned more than a century through my family. We remain fully committed to supporting Juventus’ sporting and financial success and believe there is a bright future ahead.

As the legendary Omar Sivori once said: “Here you must always fight and when it seems that all is lost, keep believing, Juve never gives up.”

Our unlisted companies delivered mixed results

Performance across our unlisted companies in 2025 was mixed, reflecting different industry dynamics, stages of development and execution outcomes. Some businesses performed very well, others faced more challenging conditions, and in a few cases, we made deliberate decisions to change our level of involvement. Overall, our private companies had a positive contribution to our portfolio.

Through our investment in Institut Mérieux, we strengthened our exposure to diagnostics, investing directly in bioMérieux in 2025. Given the company’s quality, long-term positioning and current valuation, bioMérieux represents an attractive opportunity in a sector we know well and find attractive.

Christian Louboutin delivered a solid performance in a challenging luxury market. Growth was driven primarily by women’s shoes, supported by the success of the Loubishow at the Molitor pool and strong reception of new models, including Miss Z, which contributed to market share gains.

Welltec delivered a strong year. Despite oil price volatility, the company continued to perform well, driven primarily by higher Interventions activity. Revenues reached $431 million, with $206 million of EBITDA, reflecting both operating leverage and Welltec’s market-leading position in wireline-based surgical interventions. The company also continued to strengthen client relationships and expand its presence in the Middle East.

Casavo completed a new capital increase during the year. Along with several other major shareholders, Exor chose not to participate. As a result, we are no longer shareholders in the company.

In early 2026, we exited our ownership position in GEDI Gruppo Editoriale, following a careful assessment of its long-term needs. This choice was also grounded in an evaluation of what is required for a media business to be both economically sustainable and editorially independent in today’s environment in Italy.

Our relationship with Italian newspapers spans more than a century. We have been proud owners of La Stampa for nearly 100 years and more recently of La Repubblica, which celebrated its 50th anniversary in 2026. The newspaper was co-founded by my great uncle Carlo Caracciolo who was its first publisher. We were also owners of Corriere della Sera, which turned 150 this year, for decades. We stepped in on three occasions to help secure Corriere’s future and supported its inclusion within a focused Italian media company that allowed it to perform well in recent years. Throughout this long history, we have consistently supported our media companies’ editorial independence and ensured that their journalists could carry out their work with integrity.

As I have mentioned in past letters, the newspaper industry in Italy has faced increasing structural challenges. What has become clear is that the digital transformation of the sector is no longer optional; it is the only viable path to ensure long-term sustainability.

Financial stability and self-sufficiency are essential to safeguarding editorial freedom. A newspaper supported by its readers can remain independent; that is harder to achieve if it relies on a benefactor. Since taking control, we have encouraged GEDI to accelerate its digital transformation, which we see as the key to building a sustainable future. In a media landscape increasingly shaped by technology and artificial intelligence, success requires international reach, diversified platforms and strong technological capabilities.

Our experience as the largest shareholder of The Economist Group illustrates this clearly. It continues to grow both its revenues and profits, driven by strong demand for The Economist magazine and the expansion of its enterprise subscriptions business, while successfully advancing its digital transformation. Despite the significant efforts made by GEDI, achieving a similar trajectory has proven more difficult.

This conviction led us to seek an owner able to provide GEDI with greater scale. That process resulted in an agreement with Antenna Group, a family-owned media platform operating across 22 countries in Europe, North America and Australia. Antenna manages 37 television channels and two streaming services and brings three decades of experience in building and growing media businesses with a long-term perspective.

Antenna’s plans for GEDI include the further development and internationalisation of its brands, continued investment in content and technology, while maintaining editorial independence.

La Stampa, given its distinctive local identity in Northwest Italy, will follow a separate path to ensure that it maintains that special relationship with its roots. GEDI is in the process of selling the newspaper to the media operator SAE Group, which is expected to partner with local investors from the region to preserve the voice of Turin and Piedmont.

For Exor, these transactions are about placing La Repubblica, the broader GEDI group and La Stampa into the hands best equipped to support their next phase of development. This approach is consistent with our past divestments, where our priority has always been to ensure that businesses find the best home for their long-term success.

As I mentioned last year, we have historically invested across diverse asset classes and have decided to concentrate these activities in Lingotto, our investment management company. In line with that decision, we have continued to monetise some of our financial investments with good returns.

LINGOTTO: $10 billion milestone reached through performance

We established Lingotto to pursue investments through distinct strategies, each with a clear mandate and with the objective of delivering strong long-term performance, as I have noted in the past. This approach allows our talented investors to do what they love: investing. I am pleased to see Lingotto remains faithful to these founding principles while continuing to deliver attractive returns.

Lingotto reached an important milestone at the end of 2025, nearly tripling its assets under management since its official launch in 2023 to over $10 billion. This growth reflects the disciplined application of a clearly defined set of investment strategies. Consistent with Lingotto’s purpose, the increase has come primarily from investment performance rather than capital inflows. The most notable contribution came from the returns of the Intersection Strategy led by Matteo Scolari.

The Intersection Strategy’s investments in precious metals mining (gold and platinum-group metals collectively) had the largest overall impact on performance in 2025, thanks primarily to strong metal price appreciation during the year. The strategy’s investment in Carvana, which I mentioned last year, also continued to perform well. Despite a volatile backdrop, Carvana achieved very strong operating performance throughout the year. The investment in Paramount-Skydance was also a positive contributor. The company’s financial results were secondary to the ongoing acquisition process surrounding Warner Bros. Discovery which, if completed, will create a large, new and credible competitor to Netflix.

The most notable portfolio change made in the Intersection Strategy in 2025 was an increase to the holding in Schlumberger. The Intersection team believes that energy markets will tighten significantly by the end of this decade, as planned oil projects prove insufficient to meet projected demand and new capacity shifts towards higher-cost offshore projects. Schlumberger is well positioned for this industry shift. Overall, most positions in the portfolios performed positively last year, while Ocado was a detractor.

The Horizon Strategy’s private market company investments have continued to deliver encouraging early results, as has the hedge fund exposure within the fund of funds business. The main contributors to Horizon’s performance in 2025 were investments in Neura Robotics and Jessica McCormack. In June, Neura unveiled its third-generation humanoid robots amid positive momentum in its global order book. Meanwhile, Jessica McCormack established itself as a hard-luxury brand, achieving sales growth of around 60% last year as it began international expansion with the opening of a new store in New York.

Now in its third year since inception, the Innovation Strategy’s investment performance has been led by both public and private exposure but has also grown from the onboarding of select new limited partners who share our long-term approach.

The most material contributor to Innovation’s performance was a new cornerstone investment made in the Hong Kong IPO of the world’s leading battery company, CATL. Other contributors to performance during the year included the investments in medical technology company Tempus AI, and the private cloud-based database platform, Databricks.

The Mosaic Strategy demonstrated solid initial capital deployment in 2025 as it closed its first three investments. The areas of focus have included creator economy, mobile video gaming intellectual property, and specialty finance asset originators. The team continues to develop research themes that bring together novelty and structure, along with more limited correlation to broader markets.

Lastly, Lingotto has also been deliberate in the quality of investors with whom it has chosen to partner. In that spirit, it has welcomed a select group of the world’s leading institutional investors, united by a shared commitment to advancing long-term positive societal impact in education, healthcare and philanthropy.

CASH AND CASH EQUIVALENTS

Our cash and cash equivalents increased by €1.2 billion, mainly driven by the monetisation of assets for €3.7 billion, including the Ferrari placement and reinsurance funds, and dividend inflows from our companies of €0.7 billion. This was partially offset by investments made mainly in Philips, bioMérieux and Lingotto for €1.4 billion, shareholder distributions, including buybacks, of €1.1 billion (which represented nearly 6% of our market capitalisation), and repaid €0.4 billion of borrowings net of new debt issuances.

GROSS DEBT

In October 2025, we returned to the public market, successfully pricing a €600 million ten-year bond, with a fixed annual coupon of 3.75%. This transaction allowed us to raise funds at favourable market conditions to refinance maturing debt.

The majority of our debt is made up of bonds with an average maturity of six years and an average cost of 2.8%. Most of this debt (96%) is denominated in Euro and carries fixed interest rates. We remain committed to maintaining our A- rating and will continue to prioritise a strong balance sheet, particularly in these uncertain times.

In order to strengthen our credit profile, we reduced our leverage target to 15% from 20%, reflecting a higher credit standing and commitment to strong investment-grade metrics. We have also enhanced our financial resilience and funding flexibility by more than doubling committed credit facilities to €1.1 billion and extending tenors to 3-5 years from 1-2 years.

We are simplifying our portfolio, sharpening our priorities and concentrating on our larger companies, where we believe Exor can create the greatest value. In addition to the Iveco Group and GEDI transactions, we have signed agreements to divest our stakes in Lifenet and NUO. These four transactions are expected to generate €2 billion in proceeds this year, with a total multiple of more than 1.4x on our invested capital.

I want to highlight that in each of these cases we have not only unlocked value but have also been deliberate in selecting owners with the skillset and ambition to support the next phase of these businesses’ development. Our objective has not simply been to accept the highest bid, but to ensure that these companies find the right long-term homes where they can continue to grow and thrive.

Together with the proceeds realised in 2025 as well as others to come this year, we have further strengthened our balance sheet while reducing complexity. Maintaining a strong balance sheet remains a priority for us, both defensively and offensively.

As a result, we are increasing our cash available for deployment to more than €3.5 billion, which also places us in a strong position to pursue a significant new investment similar in scale and ambition to Philips. 2026 has begun with global geopolitical and market uncertainties, so we must remain prudent.

In my recent conversations with business leaders on how they are positioning themselves in the current environment, the consistent message has been one of caution. The most forward-looking companies are choosing to reduce risk exposure, preserve capital and wait for greater clarity. This reinforces our view that now is the time to safeguard liquidity and be ready to act decisively when the right opportunities emerge.

Just as importantly, we are determined to demonstrate that Exor is capable of building and stewarding companies that are well managed and prepared for the future. Much of the work over the past year has focused on confronting challenges directly, addressing underperformance where it exists, and strengthening governance and leadership. As a result, we have emerged stronger and more resilient. That discipline will continue.

2026 also carries symbolic weight. It marks the 160th anniversary of our founder’s birth in 1866, an occasion that naturally invites reflection on durability, responsibility, and roots. Lasting success requires finding harmony between competing objectives. A company overly anchored in its past risks losing relevance; one focused only on the future risks neglecting the present. Stewardship requires holding both perspectives at once: respecting heritage while investing in innovation, valuing what has been built while preparing for what comes next.

Exor’s priorities are clear: to simplify our portfolio and concentrate on a smaller number of large companies where we can be more closely involved through governance and oversight. Finally, we will continue to deploy capital with discipline.

2026 will continue to be a demanding year. But we have confidence in the path ahead and are ready to build. We will continue to support and challenge our companies, acting as their critical friends in pursuit of lasting success.

There is an African proverb that says: “When the roots are deep, there is no reason to fear the wind.” It is a reminder that resilience is built long before it is tested. With that spirit, we look to the year ahead, ready to meet its challenges and seize its opportunities.